Imagine launching a crypto trading platform only to realize you missed a critical federal filing. For many founders, that moment comes when they learn about FinCEN registration. It is not just paperwork; it is the gateway to legally operating in the United States. If you are running a centralized exchange, a custodial wallet service, or a payment processor involving digital assets, you likely need to register as a Money Services Business (MSB). This requirement stems from the Bank Secrecy Act (BSA), and ignoring it can lead to severe penalties, frozen accounts, or even criminal charges.

The landscape has shifted dramatically since FinCEN first issued guidance on virtual currencies in 2013. By 2026, with nearly 30% of American adults holding some form of cryptocurrency, the stakes are higher than ever. Regulators are no longer watching from the sidelines; they are actively enforcing rules designed to prevent money laundering and terrorist financing. Understanding exactly what triggers this registration and how to comply is not optional-it is survival.

Who Needs to Register as an MSB?

Not every entity touching crypto needs to register. The key lies in whether your business engages in "money transmission." Under FinCEN’s definition, if you accept value from one person and transmit it to another, you are transmitting money. This applies broadly to centralized exchanges that facilitate trades between cryptocurrencies and fiat currency (like USD) or between different cryptocurrencies.

- Crypto-Fiat Exchanges: Platforms allowing users to buy Bitcoin with dollars must register.

- Crypto-Crypto Exchanges: Even if no fiat touches your system, swapping Ethereum for Solana counts as transmission.

- Custodial Wallet Providers: If you hold private keys for customers, you are safeguarding their funds and likely transmitting them upon request.

- Payment Processors: Businesses enabling merchants to accept crypto payments fall under this umbrella.

However, non-custodial wallets-where users hold their own private keys-often sit in a gray area. If your software merely helps users manage their own unhosted wallets without intermediating transactions, you might avoid MSB status. But be careful: if you add features like instant swaps or third-party funding, you cross the line into regulated territory. The distinction is thin, and misclassification is a common pitfall.

The Registration Process: What Actually Happens?

Unlike state licenses, FinCEN does not issue a formal "license" after review. Instead, it maintains a registry. You submit Form 107, the "Registration of Money Services Business," electronically via FinCEN’s web portal. The process is straightforward but requires precision.

- Gather Entity Details: Prepare legal names, physical addresses, and ownership structures. Beneficial ownership information is crucial here.

- Identify Principal Officers: List individuals with significant control over the business.

- Submit Form 107: Complete the online form. There is no fee for federal registration itself.

- Maintain Active Status: Update your registration within 180 days of any material change, such as a new address or change in ownership.

While the federal step is simple, do not mistake it for the end of your compliance journey. FinCEN registration is just the entry ticket. The real work begins with implementing an Anti-Money Laundering (AML) program that meets federal standards.

Beyond Federal: The State Licensing Maze

Federal registration is necessary but not sufficient. In the U.S., financial regulation is dual-layered. While FinCEN handles federal AML oversight, states control who can operate money transmission services within their borders. This means you must obtain a Money Transmitter License (MTL) in every state where you have customers or operations.

| Requirement Type | Authority | Purpose | Cost Estimate |

|---|---|---|---|

| MSB Registration | FinCEN (Federal) | AML/CFT Oversight | $0 (Free) |

| Money Transmitter License | State Regulators | Operational Permission | $5k - $10k per state |

| BitLicense | New York DFS | Specialized NY Approval | $50k+ application + annual fees |

New York stands out with its BitLicense, a notoriously rigorous and expensive approval process. Other states may have varying requirements, bonding amounts, and insurance mandates. Navigating all 50 states individually is cost-prohibitive for most startups. Many choose to partner with already-licensed entities or use banking-as-a-service providers who handle the licensing burden, though this introduces counterparty risk.

Core Compliance Obligations: KYC, AML, and Reporting

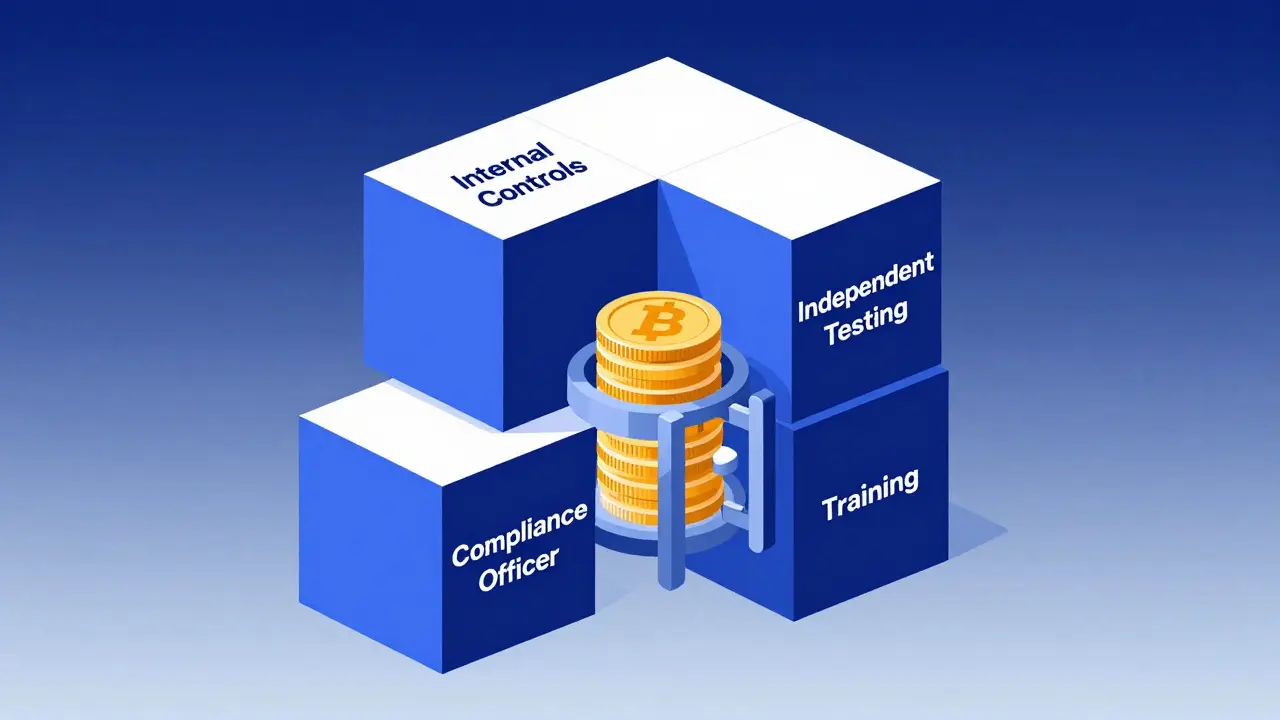

Once registered, you must build a robust compliance infrastructure. FinCEN expects four pillars in your AML program:

- Internal Controls: Policies and procedures tailored to your specific risks. Generic templates rarely pass audits.

- Independent Testing: Regular audits by third parties to verify your controls work.

- Designated Compliance Officer: A senior employee responsible for day-to-day adherence.

- Ongoing Training: Staff must understand red flags for money laundering and sanctions evasion.

Know Your Customer (KYC) procedures are central to this. You must verify the identity of every user before allowing significant transactions. This involves collecting government IDs, proof of address, and sometimes source-of-funds documentation. For institutional clients, beneficial ownership verification is mandatory.

Transaction monitoring systems must flag suspicious patterns. Are users structuring deposits to stay below reporting thresholds? Is there rapid movement of funds through multiple wallets? These behaviors trigger Suspicious Activity Reports (SARs), which must be filed with FinCEN within 30 days of detection. Failure to file a required SAR is a serious offense.

Recent Regulatory Shifts and Future Outlook

The regulatory environment is evolving rapidly. Recent proposals aim to classify convertible virtual currencies (CVC) more explicitly as monetary instruments under the BSA. This would tighten recordkeeping requirements, especially for transactions involving unhosted wallets or jurisdictions flagged by FinCEN.

In 2023, FinCEN targeted mixing services, highlighting its focus on obfuscation tools. As technology advances, regulators are adapting. Expect increased scrutiny on decentralized finance (DeFi) protocols if they exhibit characteristics of traditional intermediaries. The trend is clear: transparency is becoming non-negotiable.

Looking ahead, there is talk of a federal framework that could streamline state licensing. However, until Congress acts, the patchwork remains. Companies must prepare for ongoing changes, including potential data localization rules and enhanced customer due diligence standards.

Practical Steps for New Entrants

If you are planning to launch, start early. Compliance takes time and money. Here is a realistic checklist:

- Consult Legal Experts: Hire attorneys specializing in fintech and crypto law. Do not rely on generalist advice.

- Map Your Jurisdictions: Decide which states to target initially. Focus on high-volume areas first.

- Select Technology Partners: Choose KYC providers and transaction monitoring platforms with proven track records.

- Build Financial Reserves: Budget for licensing fees, bonding, insurance, and ongoing compliance staff.

- Document Everything: Keep detailed records of policy decisions and training sessions. Auditors will ask.

Remember, compliance is not a one-time task. It is a continuous cycle of assessment, implementation, and improvement. Treat it as a core part of your business model, not an afterthought.

How long does FinCEN registration take?

FinCEN registration is typically immediate upon submission of Form 107. However, obtaining state Money Transmitter Licenses can take 6 to 18 months depending on the jurisdiction and completeness of your application.

Do decentralized exchanges (DEXs) need to register?

Currently, pure DEXs without a central operator often avoid MSB status. However, if a team controls smart contracts or provides liquidity pools in a way that constitutes transmission, regulators may argue otherwise. The line is blurry and subject to enforcement actions.

What happens if I fail to register?

Penalties include civil fines up to $25,000 per violation, asset forfeiture, and potential criminal prosecution. Banks may also cut off your fiat rails, effectively shutting down your business.

Is FinCEN registration enough to operate nationwide?

No. FinCEN registration satisfies federal AML requirements, but you still need state-level Money Transmitter Licenses to legally operate in each state. Operating without state licenses exposes you to local enforcement actions.

How often must I update my FinCEN registration?

You must update your registration within 180 days of any material change, such as a change in principal officers, ownership structure, or physical address. Annual renewals are not required, but accuracy is mandatory.

Andrew Schneider

July 19, 2026 AT 16:26Eric Braddock

July 21, 2026 AT 09:03Ray Arney

July 21, 2026 AT 20:56Alicia Hull

July 22, 2026 AT 13:21Tracy Marshall

July 24, 2026 AT 00:34Guy Davis

July 25, 2026 AT 09:58Lisa Chong

July 26, 2026 AT 05:25Heather Austin

July 26, 2026 AT 18:53Ran Tao

July 28, 2026 AT 18:07Nick G

July 30, 2026 AT 15:37Nick Wengel

July 31, 2026 AT 05:50Johan Otto

July 31, 2026 AT 16:59Anuj Kashyap

August 1, 2026 AT 01:47KEITH WONG

August 1, 2026 AT 12:46Natalie Lucas

August 1, 2026 AT 21:03Curtis Johnson

August 2, 2026 AT 13:16Steven Briggs

August 2, 2026 AT 23:50